There is a specific kind of anxiety that hits you when your dog’s muzzle starts turning gray.

You watch them take a little longer to stand up after a nap. You notice a new lump while scratching their belly. And suddenly, the “Big Vet Bill” isn’t just a hypothetical fear anymore—it feels like a looming inevitability.

For the last 20 years, I’ve navigated the “sugar face” years with multiple dogs. And I know exactly what happens next. You panic. You hop online at 2 AM and Google “pet insurance for 12-year-old dog.” You see a quote for $180 or $250 a month, and you wince. But you think, “I have to do it. I can’t let money be the reason I can’t save them.”

But here is the hard truth that insurance companies won’t tell you in those heartwarming commercials: For senior dogs, insurance is often a financial trap.

Because of “pre-existing condition” clauses, you might end up paying thousands in premiums, only to have your claims denied exactly when you need them most.

I got tired of seeing caring owners drain their savings on policies that don’t pay out. So, I built a tool to help you run the math yourself.

What This Calculator Does

- Estimates exclusion risk (how likely “pre-existing conditions” gut your coverage).

- Compares premiums vs a savings pot so you can see opportunity cost.

- Gives a plain-language verdict: “Good Bet,” “Safety Net,” or “Likely Waste.”

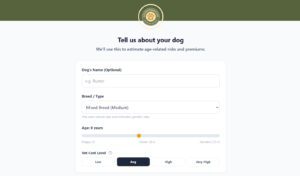

The Golden Paws Insurance Forecaster

How to Use It

- Answer honestly about your dog’s history (this is where “exclusions” come from).

- Compare the premium to what you could save monthly instead.

- Use the verdict as a decision aid — not a rule. Your budget and risk tolerance matter.

The “Panic Buy” Problem

Most people buy pet insurance for puppies, which makes sense. A puppy is a blank slate. They haven’t limped, they haven’t had an ear infection, and they haven’t been diagnosed with anything. Insurance companies love puppies because the risk is low (for a while), and the premiums are cheap.

But senior dog owners usually buy insurance in response to a scare. Maybe your Lab started limping on its back leg. Maybe your Rottweiler has a new heart murmur.

You buy the policy seeking a safety net. But in the fine print of that policy lies the “Pre-Existing Condition” exclusion. It essentially says: If your dog showed signs of this issue before you signed up, we will never pay for it.

And “signs” is interpreted broadly. That limp? That’s pre-existing arthritis. That itchiness? Pre-existing allergies.

If insurance isn’t the right answer, preparedness still matters — tools like the Emergency ID System help in real emergencies.

Why I Built This Tool

I realized that we needed a way to calculate Exclusion Risk. We needed a “Truth Serum” for pet insurance quotes.

This app isn’t designed to sell you insurance. In fact, for many of you with dogs over age eight, it’s going to tell you not to buy it.

It breaks down the decision into three logical steps that your emotions usually try to skip:

1. The Exclusion Friction Score

The calculator asks you about your dog’s history—honestly. Does she have dental disease? Has he torn a cruciate ligament before?

If you check “Cruciate History,” the app knows about the “Bilateral Exclusion” rule (which means that if one knee goes, insurers often won’t cover the other). It calculates a friction score that estimates the probability that your claims will be denied.

2. The “Savings Pot” Showdown

This is my favorite feature. We all look at the monthly premium—say, $140/mo—and think, “I can squeeze that in.”

But we rarely calculate the Opportunity Cost.

The app runs a 5-year simulation. It asks: What if, instead of sending that $140 to an insurance company, you put it into a dedicated High-Yield Savings Account (HYSA) for your dog?

The results are often shocking. By Year 3, many owners would have a “Self-Insurance” pot of $4,000 to $6,000 available in cash. That is money you control. Money that never gets denied because of a “waiting period.” Money that can be used for prescription food, hydrotherapy, or supplements—things insurance often ignores.

3. The Reality Check

Finally, the app compares your projected costs against real-world vet prices for your dog’s size. It shows you exactly what “Breaking Even” looks like.

If the math says you need $1,200 in claims every single year just to break even, you have to ask yourself: Is my dog likely to have a $1,200 catastrophe every year that ISN’T related to his pre-existing arthritis?

When IS Insurance Worth It?

I am not anti-insurance. I actually carry it on my younger dogs. The calculator will tell you if insurance is a “Good Bet” or a “Safety Net.”

This usually applies if:

- Your senior dog has a remarkably clean medical record (a “unicorn” senior).

- You are financially “risk-averse”—meaning you would rather overpay $2,000 in premiums over 5 years than risk a single surprise $5,000 bill on a Tuesday.

Insurance Forecaster FAQ

Is pet insurance ever worth it for senior dogs?

Sometimes — especially when the dog has a clean medical record, you enroll before symptoms appear, and the premium still makes sense relative to your savings ability.

Why do “pre-existing conditions” matter so much?

Because many older-dog claims trace back to earlier symptoms. If a condition can be argued as pre-existing, coverage can be reduced or denied — even when you pay premiums for months.

If the calculator says “Likely Waste,” what should I do?

Use the same monthly premium to build a vet savings pot, and focus on preparedness tools and prevention spending that reduces injury risk and surprise costs.

A Better Plan for the Golden Years

If you run the numbers above and get a “Likely Waste” verdict, don’t feel guilty. You aren’t failing your dog; you are being smart with your resources.

Take that premium money and redirect it. Open a separate savings account named after your dog. Set up an auto-transfer for the exact same day you would have paid the insurance bill.

If Insurance Isn’t Worth It, Do This Instead

If the verdict leans “Likely Waste,” you’re not failing your dog — you’re switching to a plan that actually works for many seniors.

- Start a vet savings pot with the same monthly amount you’d pay in premiums.

- Build an emergency profile so caregivers and vets get the right info fast.

- Prioritize prevention spend (mobility support, dental timing, joint care, fall prevention).

In six months, you’ll have an emergency fund. In two years, you’ll have a war chest. And best of all, you’ll have the freedom to make medical decisions based on what your dog needs, not what a claims adjuster decides to approve.

Give the calculator a try. It takes about two minutes. It might just save you enough money to buy a really, really good orthopedic bed (and a lot of treats).

Next Steps

Whether you buy insurance or not, preparedness still matters for senior dogs.

Is Pet Insurance Worth It for Older Dogs? (The Honest Calculator)

Don't panic buy. Our free calculator models premiums vs. exclusions to show if pet insurance is a safety net or a waste of money for your senior dog.

Price: 0.00

Operating System: web

Application Category: UtilitiesApplication